Why Big Data analytics has become the next battlefront in insurance

Higher disruptive waves are rolling in on the insurance sector and their pace is accelerating. It took 15 years for insurers to sell direct to their customers, and to price and issue policies online while competing on price comparison websites. Many still have not achieved it.

But the waves have accelerated and insurers now need to simultaneously:

- Refocus their entire customer strategy to make it smartphone centric.

- Adapt to Usage-Based Everything, which not only includes Usage-Based Insurance (UBI) but also an adaptation to the sharing economy.

- Update their models and capabilities to be ready for ADAS and, soon, highly autonomous vehicles (HAVs).

Each disruptive wave is linked to the next, and they are happening in order. However, with the rapid digitalisation of the industry, these waves are accelerating and superimposing. They carry with them undercurrents that can form powerful competitive advantages capable of wiping out unprepared stakeholders.

Each disruptive wave is linked to the next, and they are happening in order. However, with the rapid digitalisation of the industry, these waves are accelerating and superimposing. They carry with them undercurrents that can form powerful competitive advantages capable of wiping out unprepared stakeholders.

Big Data analytics is one of those undercurrents. It started to grow in importance as telematics insurance emerged, and is now turning into underwriters’ main priorities.

Today the majority of insurers using telematics in their pricing are limiting their analytics to three or four criteria. The process of determining what is predictive of risk is complex and expensive. It also requires knowledge in data science and the appropriate tools.

As part of our research for the Connected Insurance Analytics report, we have interviewed more than 60 insurers globally. When asked about the most challenging part of offering Usage-Based Insurance, three items recurred most often:

- Flexible IT infrastructure came third

- The shortage of data scientists came second

- But the most common issue was the lack of understanding about how to extract value from driving data

UBI devices can generate a vast array and quantity of data, including location, acceleration (including crash detection and possibly reconstruction), as well as OBD data in real-time. To that, the insurer will often look at adding external datasets that will provide context to the vehicle data.

Unsurprisingly, it is a challenging task to manage and process this data with traditional underwriting platforms. The analytics output is also a challenge; insurers have to handle the information in order to not only assess risk profiles, price policies and give discounts, but also to trigger emergency assistance and detect fraud … all this whilst ensuring all data regulations are followed.

In fact Paul Stacy, Founder of Wunelli and director at Lexis Nexis commented recently that “there was no way insurers could keep up with the growing variety of aftermarket and OEM data sources”.

At the centre of this process is advanced data analytics – the ability to extract the most valuable information from a variety of real-time data sources and apply autonomous algorithms to discover risk predictive patterns.

The results are proven; Larry Thursby, Vice President at Nationwide mutual insurance told PTOLEMUS: “We’ve now built our own proprietary scoring program that supports discounts of up to 40%”.

The strategies from the biggest players can be split into three tiers. Most of the insurers today have done nothing or very little. This includes researching and maybe trialling telematics or apps in order to investigate how to use the new types of information.

Some of the large insurance groups, such as Allstate and Progressive, have built on their early footsteps in UBI and ramped up advanced analytics functions internally. Progressive has started a vast recruitment plan to attract data scientists. Allstate has created a subsidiary called Arity, a new entity that will collect data on drivers and sell analytics products to third parties. Generali also made a strong move by acquiring MyDrive, a British analytics provider with early footsteps in smartphone UBI.

The third tier is maybe the least visible but the busiest: Hundreds of insurers trialling UBI with Telematics Service Providers (TSPs) are now hoping they will be able to benefit from Big Data analytics. Granted, some have the capability, but as we have seen in our analytics, not all TSPs are Advanced Analytics providers as well.

This is why we published the Connected Insurance Analytics (CIA) report. It addresses the priorities of all insurance companies, not just the telematics insurance brokers. The CIA report is a step-by-step guide to Advanced Analytics. It describes, analyses and illustrates the process by which top analytics companies take raw driving data and transform it into real-time, individual risk profiles.

The research is based on our analysis of the pricing and data management policies of the 27 largest UBI programmes, including Admiral, Allianz, Allstate, American Family, AXA, Generali, Desjardins, Direct Line Group, State Farm, The Hartford, UnipolSai, Uniqa and Zurich.

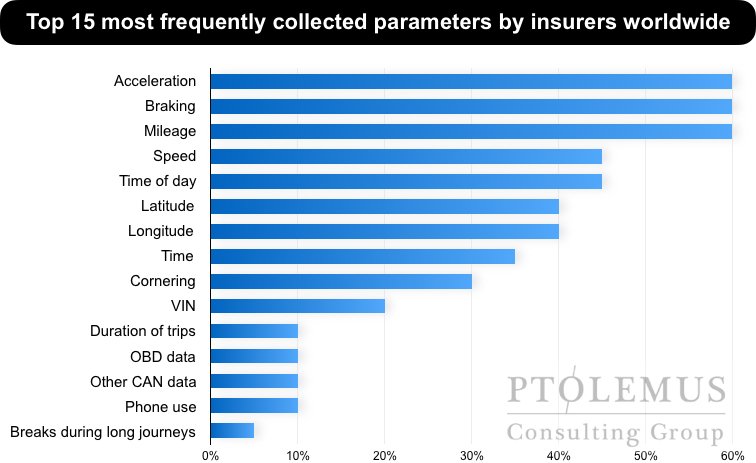

PTOLEMUS analysed what data was collected by these programmes, and how frequently that information was used to score drivers. Acceleration, braking and mileage came top, perhaps not surprisingly, but the range of factors is much wider and illustrates the difficulty in choosing the correct criteria.

To offer a fair driving score, PTOLEMUS believes insurers need to have a deep understanding of the driving conditions. Adding contextual data, such as road type, speed limit, relative speed limit, risk profile of each road and historical crash data, is a necessary step to effectively judge the risk profile.

Download 20 best practice in Advanced Analytics

In the world of Big Data, insurers have to very quickly evolve to compete on the analytics level. The increasing speed, volume and complexity of the data available will force underwriters to use advanced analytics methods.

Not all solution providers are ready in the same way, and with more announcing their analytics capabilities, we expect the differentiating factors will include their ability to enrich the data with context and to manage large samples of driving data calibrated with large samples of loss data, or at least detailed crash data.

Download the free Connected Insurance Analytics report abstract

Related study

Connected Insurance Analytics Report

While the UBI market is continuously growing and evolving faster than ever, at its core is the capability of the insurers and of their service...

Related industry